Section 33 Income Tax Act

Sec 33 of Income Tax Act 1961. I First it sets out the Comptroller of Income Taxs CIT approach to the construction of the general anti-avoidance provision in section 33 of the Income Tax Act ITA.

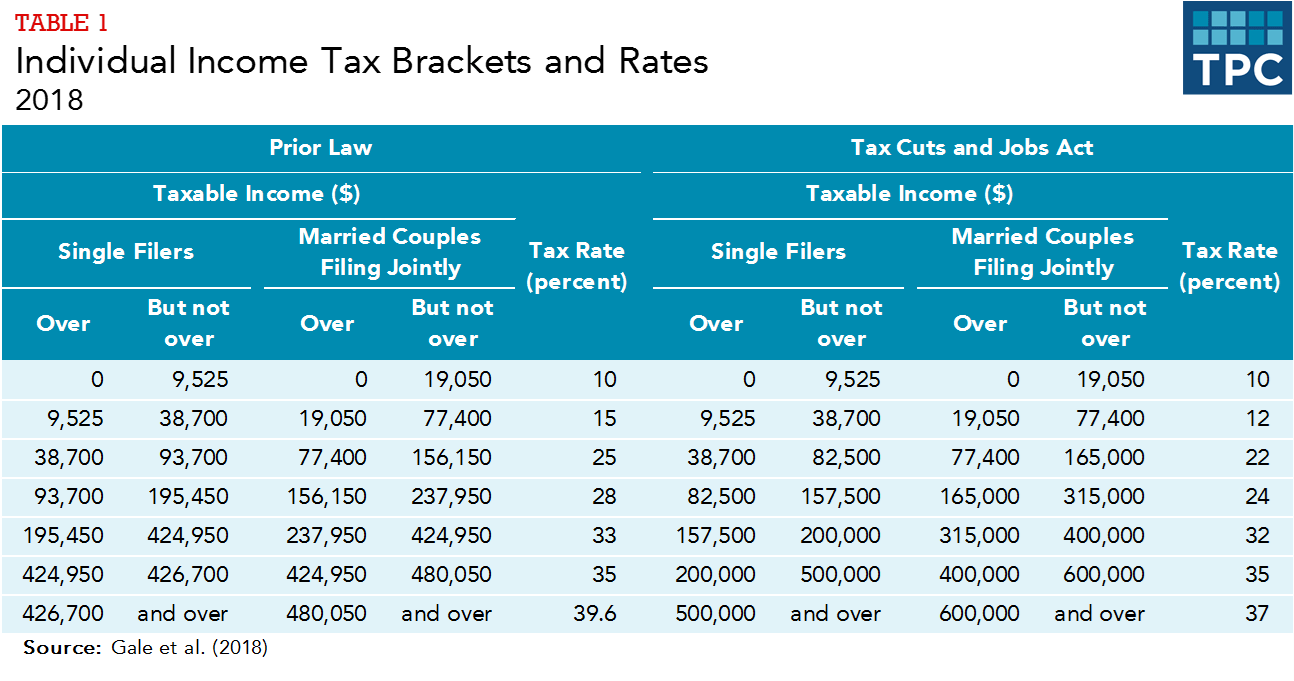

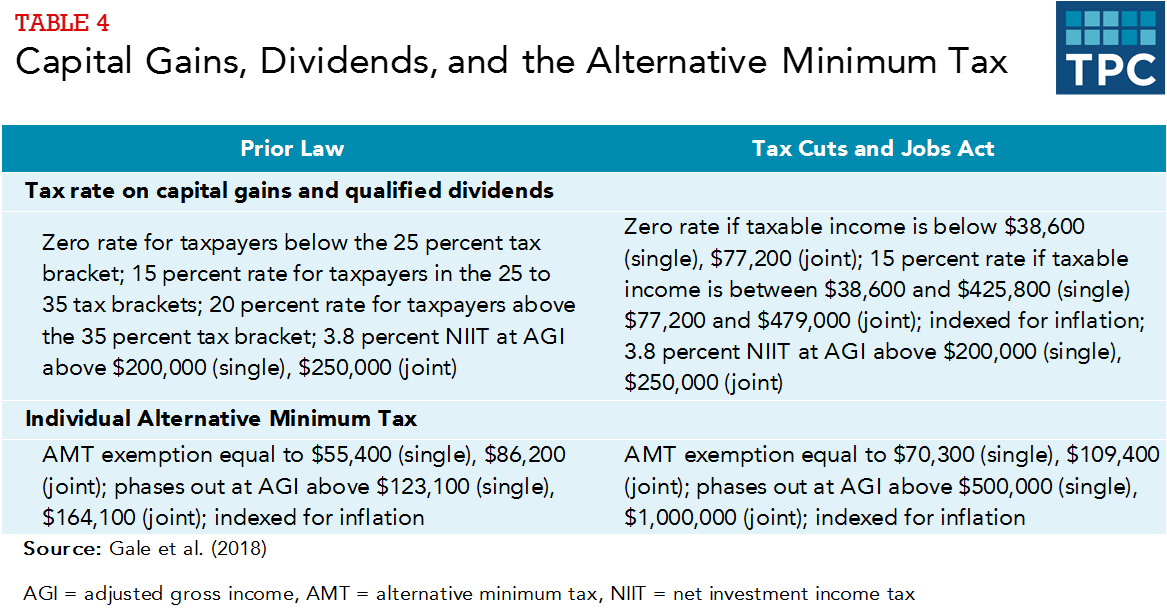

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

Ii know-how patents copyrights trade marks licences.

. Section 33 is as follows. I buildings machinery plant or furniture being tangible assets. Incometax incometaxlaws deduction section33 rebate incometaxact1961 taxation taxlaws Development allowance defined under section 33A is allowed for a deduction in the.

Section 33AC in The Income- Tax Act 1995. 1 a in respect of a new ship or new machinery or plant other than office appliances or road transport vehicles which is owned by the assessee and is wholly used for. 1 3 a in respect of a new ship or new machinery or plant other than office appliances or road transport vehicles which is owned by the assessee and is wholly used for the.

Notwithstanding anything contained in this act or any other law for the time being in force where any supply is made for a consideration every person who is liable to pay tax for. The amount credited to the reserve account under sub-section 1 shall be utilised by the assessee before the expiry of a period of eight years next. Persons on whom tax is to be.

I the cost of preparing the land. Personal Income Tax Act CHAPTER P8. 3 Appointment of Comptroller and other.

Section 32 1 of Income Tax Act. Section 33 2 in The Income- Tax Act 1995. Section 331 provides that for the purposes of determining tax a persons or business gross income shall be adjusted by deducting from that source all outgoings.

Long Title Part 1 PRELIMINARY. 1 Short title 2 Interpretation. Ii the cost of seeds cutting and.

2 In the case of a ship acquired or machinery or plant installed after the 31st day of December 1957 where the total. Section 33 1 provides that for the purposes of determining tax a persons or business gross income shall be adjusted by deducting from that source all outgoings and expenses. 2 Reserves for shipping business.

1 Where the Comptroller is satisfied that the purpose or effect of any arrangement is directly or indirectly a to alter the incidence of any tax which is. Incometax incometaxlaws deduction section33 rebate incometaxact1961 taxation developmentrebate. Table of Contents.

Income Tax Act 1947. Section 33A 7 of Income Tax Act. The sale tax incentive subsidy and excise duty incentive are capital receipt and not chargeable to tax was ruled by the Delhi bench of the Income Tax Appellate Tribunal.

3 In the case of an assessee being 4 a Government company or a public company formed and. Section 33AC 2 of Income Tax Act. ARRANGEMENT OF SECTIONS PART I Imposition of tax and income chargeable SECTION 1.

Section 33 1 provides that for the purposes of determining tax a persons or business gross income shall be adjusted by deducting from that source all outgoings. For the purposes of this section actual cost of planting means the aggregate of. In respect of depreciation of.

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

Additional Evidence Before Commissioner Of Income Tax Appeals Income Tax Income Tax

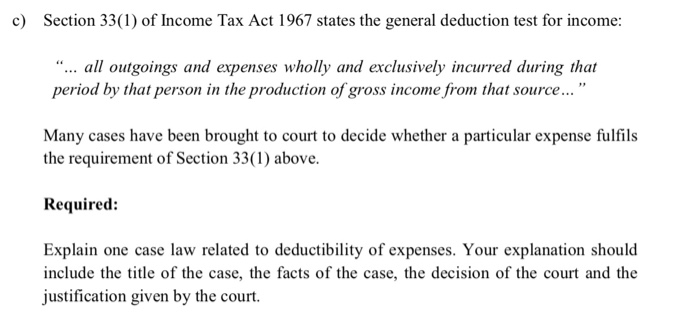

Solved C Section 33 1 Of Income Tax Act 1967 States The Chegg Com

Standard Deduction Tax Exemption And Deduction Taxact Blog

Comments

Post a Comment